Below is our summary of the latest news developments of the past week and their implications for CRE, curated by LightBox Analysts

The Weekly LightBox Perspective

After a month of political gridlock and mixed economic signals, markets found plenty to cheer about last week from easing trade tensions to a second fed cut. Yet under the surface, a new wave of corporate layoffs points to a weakening labor market that could portend trouble ahead. Meanwhile, LightBox data shows most CRE assets are appreciating with capital attracted to multifamily and retail.

1. The Fed Cuts a Second Time, Now with an Eye on Jobs

The Federal Reserve delivered its second consecutive 25-basis-point rate cut of the year last week, bringing the federal funds rate to 3.75%–4%, even as inflation remains elevated at 3% year over year. Chair Powell acknowledged that “the downside risks to employment appear to have risen,” marking a notable shift in tone toward protecting jobs rather than tightening against inflation. Still, Powell cautioned that another rate cut in December is not guaranteed, calling this a time to “slow down” amid data uncertainty worsened by the ongoing federal shutdown.

LightBox Take: The cut is more of a psychological boost than a game-changer, but lower short-term rates will help at the margins by easing some financing costs. . Rate relief supports liquidity and confidence, yet underwriting will stay tight until long-term yields move meaningfully lower. “The Fed is worried that layoffs will increase sooner and faster than hiring will accelerate,” observed Ryan Severino, chief economist and head of U.S. research at BGO, “and in cutting rates, they’re trying to head that off at the pass.” The cut is a modest but welcome tailwind for year-end lending and investment activity, keeping the market momentum of September and October on track.

2. Beyond the Headlines: LightBox Data Shows Most CRE Assets Gaining Value

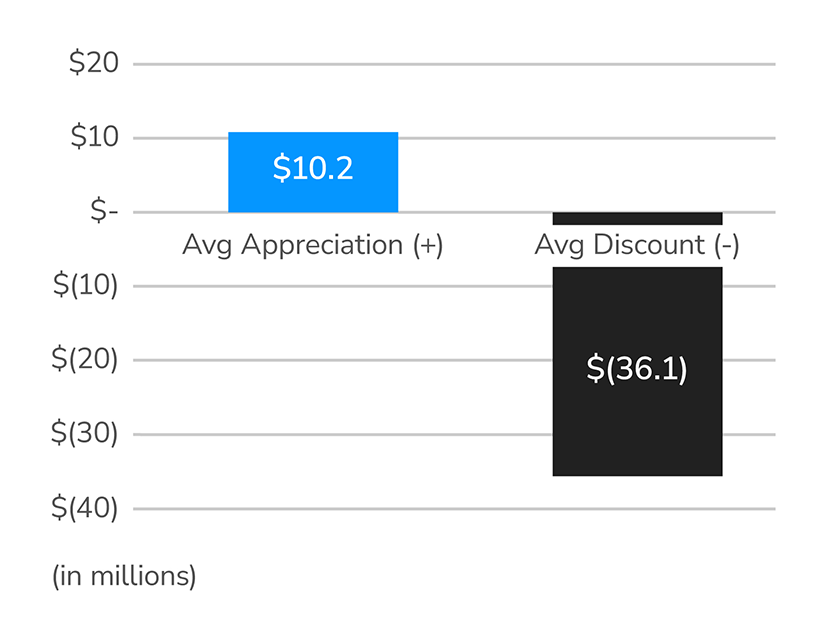

While headlines often spotlight distress and pricing resets, LightBox data shows most properties are still appreciating. Of the 970 September closings tracked by the LightBox’s Transaction Tracker, ranging from a $200K Ohio retail sale to a $1.6B multi-state portfolio, 70% sold above prior purchase prices, while 29% sold at a discount. The average appreciation across all asset classes was $10.2M, compared to an average loss of $36.1M on discounted sales.

LightBox Take: Despite talk of buyers’ remorse, especially in multifamily, our data shows transactions for assets purchased at $60-$75M in 2018 or 2019 that just closed in the range of $90–$100M. Office values remain under pressure, but capital continues to migrate toward stronger-performing retail, multifamily, and industrial sectors. With two rate cuts already on the books and more likely ahead, momentum is building. As Jay Neveloff, partner and chair of U.S. real estate at HSF Kramer, told Commercial Observer, “2026 is going to be a terrific year for transactions, and some will be opportunistic, and some will be painful.”

3. Big-Name Layoffs Signal Cooling Hiring Momentum

Major employers are broadening their job cuts, underscoring a cooling labor market. Amazon announced it will eliminate approximately 14,000 corporate jobs, accounting for 4% of its white-collar workforce, citing AI and cost-efficiency moves. Target will cut around 1,800 corporate roles, roughly 8% of its corporate staff, after stagnant sales. Meanwhile, General Motors revealed 1,700 layoffs, primarily tied to slower EV demand and regulatory pressures. These cuts add to the nearly one-million layoffs already logged this year, and they deepen concerns about job momentum entering the year-end

LightBox Take: A labor market losing steam shifts the balance for the Federal Reserve, putting more wind in its sales to trim rates further. The downside is that slower wage growth and weaker hiring could weigh on consumer spending in the retail sector and create potential recessionary headwinds.

4. A Rare Win in Chicago’s Office Market with Data Center Conversion

In one of Chicago’s most notable adaptive reuse deals, a venture of Mike Reschke’s Prime Group and Quintin Primo’s Capri Investment Group sold the former Cboe Global Markets headquarters at 400 South LaSalle Street for $40 million. The deal was notable for closing at more than triple the $12 million that owners paid last year. The buyer, Legacy Investing, plans to convert the 385,000-square-foot Loop property into a 33-megawatt data center slated to open in late 2026 amid surging demand for digital infrastructure.

LightBox Take: This is a rare, profitable flip in Chicago’s office market, and an unconventional one. Office-to-data-center conversions remain difficult, but when the logistics align, particularly access to reliable power, fiber, and structural capacity, they can be highly compelling. Reschke and Primo created significant value by securing power upgrades, evidence that a struggling asset sited in a strong connectivity corridors can find new life serving the rapidly expanding data-infrastructure economy.

5. Fed Shutdown Stalls HUD Operations, Multifamily Projects Face Growing Delays

The federal shutdown has halted most HUD operations, with about 71% of staff furloughed and only essential functions continuing. The Federal Housing Administration will close multifamily mortgages already under firm commitment but is not accepting new applications. Funding for public housing and Section 8 programs has been obligated through November, but prolonged disruption could threaten renewals and contract payments. The National Multifamily Housing Council notes that the longer the standoff continues, the greater the risk to multifamily financing stability.

LightBox Take: For environmental consultants supporting HUD lending programs, federal shutdowns are a real operational test. Environmental due diligence, appraisals, and underwriting tied to HUD deals could face cascading delays. Still, as funds remain available for near-term obligations, the immediate impact is limited so far, but if the shutdown continues, it could disrupt future project pipelines.

Did you know?

The weighted average number of non-disclosure agreements (NDAs) per broadcasted property listing:

169

Top 3 Asset Classes:

Multifamily: 221

Retail: 139

Industrial: 138

Source: LightBox RCM platform

📅 The Week Ahead

|

Mon 11/3 |

→ |

Construction spending |

|

Mon 11/3 |

→ |

Job openings |

|

Wed 11/5 |

→ |

ADP employment |

|

Thurs 11/6 |

→ |

U.S. Productivity and initial jobless claims |

|

Fri 11/7 |

→ |

U.S. employment report |