For the first time this year, commercial real estate’s momentum appears to have hit a speed bump.

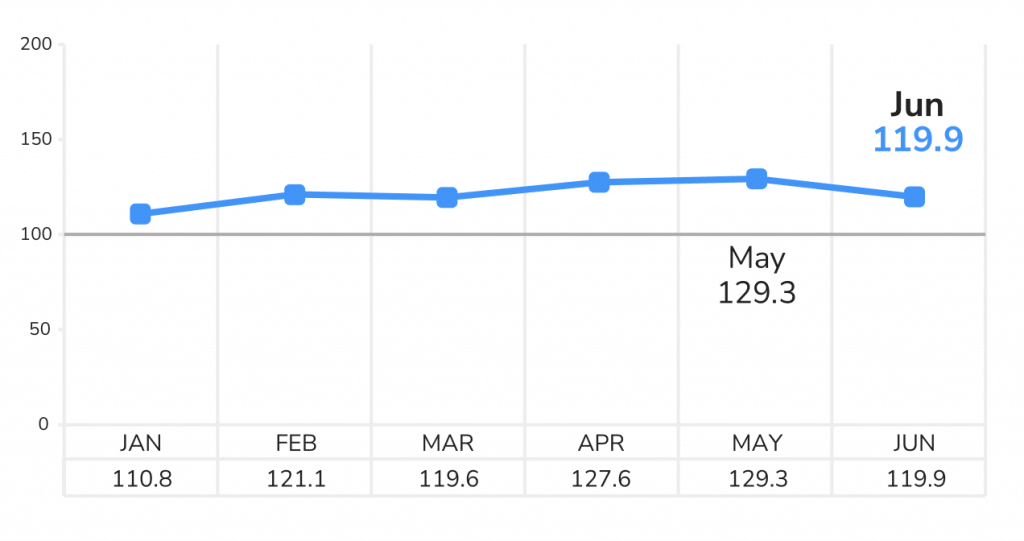

After six consecutive months of triple-digit readings, the June LightBox CRE Activity Index declined to 119.9, down 7% from May’s 2026 high of 129.3. While activity remains well above historical norms and continues to outpace June 2025, June marks the first month this year in which all three components of the Index—commercial property listings, Phase I Environmental Site Assessments (ESAs), and lender appraisals—moved lower simultaneously.

The decline doesn’t necessarily signal a market reversal. Instead, it reflects a market grappling with a rapidly changing macroeconomic landscape, where geopolitical uncertainty, elevated interest rates, and volatile Treasury yields are beginning to influence transaction activity.

A Different Kind of Slowdown

Until now, the market had demonstrated remarkable resilience with strength in listings and environmental due diligence consistently offsetting weaker lender appraisal activity, allowing the overall Index to maintain steady gains despite higher borrowing costs. June broke that pattern.

Commercial listings declined 6% from May, marking the second consecutive monthly decline after reaching a yearly high in April. Phase I ESA activity slipped just 1%, ending a four-month streak of increases but remaining above year-ago levels. The sharpest pullback came from lender-driven appraisals, which dropped 20% month over month as financing markets reacted to shifting Treasury yields and a more hawkish tone from the Federal Reserve.

While one month does not establish a trend, seeing all three leading indicators move in the same direction is noteworthy.

Macro Conditions Finally Begin to Show Up in CRE

Commercial real estate has weathered an impressive number of external shocks over the past year that have repeatedly tested investor confidence including, higher interest rates, persistent inflation concerns, and global instability. Despite those pressures, transaction pipelines remained relatively healthy throughout much of the quarter. Much of the activity reflected in June likely originated weeks or even months earlier, underscoring the lag between macroeconomic events and commercial real estate transactions.

If financing markets stabilize and geopolitical tensions ease, June may ultimately prove to be nothing more than a temporary pause. If uncertainty persists, however, this month’s pullback could represent the first indication that macroeconomic headwinds are beginning to slow deal activity more meaningfully.

Lending Activity Remains the Variable to Watch

Among the Index’s three components, lender appraisals continue to provide one of the clearest windows into transaction sentiment. Appraisal activity is directly tied to financing decisions, making it particularly sensitive to changes in borrowing costs. June’s 20% decline reflects lenders becoming more cautious as Treasury yields fluctuated throughout the month.

The encouraging news is that broader lending activity continues to recover compared to last year. Commercial mortgage originations remain significantly higher than 2025 levels, and banks have gradually returned to the market after several years of reduced activity. Rather than signaling a retreat from lending, current conditions suggest lenders are becoming increasingly selective—favoring high-quality sponsors, durable income streams, and well-positioned assets while remaining disciplined on underwriting.

Why This Matters for Investors and Brokers

For commercial real estate professionals, June’s Activity Index reinforces an important reality: today’s market is being driven by selectivity rather than broad-based momentum.

Investors continue to pursue opportunities, but underwriting assumptions are becoming more disciplined. Brokers are still bringing assets to market, although listing activity has moderated after reaching its spring peak. Environmental due diligence remains relatively healthy, suggesting transactions continue to move forward even as financing conditions tighten.

Taken together, the data points to a market that remains active. One where execution, pricing, and financing matter more than ever.

Looking Ahead

The first half of 2026 has consistently exceeded expectations, with the LightBox CRE Activity Index remaining above its historical baseline every month. June’s decline is the first meaningful interruption to that momentum, but it is far from conclusive evidence of a broader slowdown. Whether this represents a temporary pause or the beginning of a more sustained moderation will depend on how markets respond over the coming weeks. Inflation data, Treasury yields, labor market conditions, and geopolitical developments will all influence transaction activity heading into the second half of the year. For now, the message is clear: commercial real estate remains resilient, but the market is entering a period where every new data point carries greater significance than it has all year.

Read the full June LightBox CRE Activity Index for a deeper look at the trends shaping commercial real estate, including market drivers, economic analysis, lending conditions, and our outlook for the months ahead.

For more information about this report or the data, email insights@lightboxre.com