The commercial real estate (CRE) market faced another month of conflicting signs on the economy, the labor market, and consumer spending, and managed to hold onto the momentum of the past several months. News of an early August interest rate uptick in Japan coupled with disappointing employment data spooked Wall Street investors into a selloff that sent shock waves through the industry. Fortunately, the unrest was short-lived and did little to dampen the momentum that has been building in the LightBox CRE Activity Index since March.

The Index, an aggregation of daily transactions over the LightBox network, measures shifts in property listings, valuations, and environmental due diligence. Given the expected seasonal slowness of a typical August, combined with the stock market scare, the August CRE Activity Index did not fall as dramatically as it could have. Due to the renewed optimism stemming from Federal Reserve Chairman Powell’s declaration that the time for the long-awaited interest rate cuts has finally arrived, the Index is heading into what could well be a strong September and Q4 to finish out 2024.

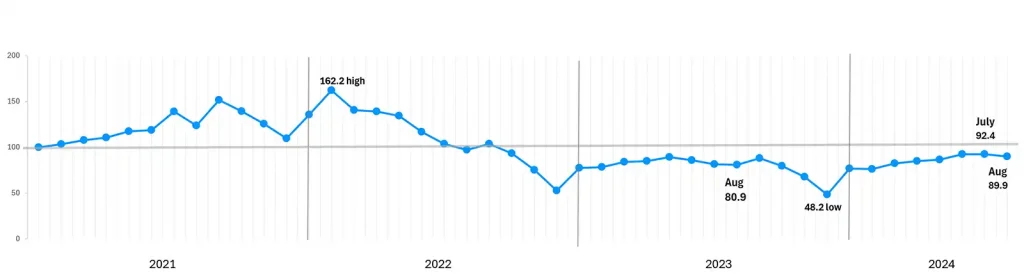

August Index Reflects Notable YoY Uptick

While August’s Index of 89.9 broke the five-month trend of steady, yet modest increases that began in March, it came in just 2.5 points below July’s 92.4. The decline could well have been more severe had the early August stock sell-off been more prolonged, the latest inflation data been less convincing, or economic data stirred up recessionary concerns. None of those developments took shape. Instead, the volume of properties listed for sale declined moderately, as expected.

This slight decline was neither concerning nor surprising considering that sellers are more likely to move assets into play after the summer season winds down. Momentum from the environmental due diligence and appraisal sectors continued in August, likely from projects already in the works. More telling (and more promising) is that August’s index landed a solid 9 points above this time last year when the Index sat at 80.9. This year-on-year uptick reflects strong improvements in all three components of the index outperforming activity in last year’s more tepid market.

Monthly LightBox CRE Activity Index (January 2021 – Present)

NOTE: The gray horizontal line indicates the Q1 2021 monthly average. The LightBox CRE Activity Index is based on changes in environmental due diligence (measured by Phase I ESA volume), commercial property listings, and valuation market activity indexed to a baseline (Q1 2021 monthly average =100) to give market watchers a pre-slowdown basis of comparison. The index is normalized to account for variations in the number of business days per month.

August Outperforms Historical Benchmarks

From a historical perspective, August’s 89.9 is well above one year ago, and just below where the CRE market stood in July. The latest 12-month moving average of 80.4 could rise if velocity builds as expected in the final months of 2024. Notwithstanding another unexpected market scare, the Index should continue on a path of steady increases as the market digests the first round of rate cuts and the CRE investment and lending sectors respond.

AUGUST 2024: Current Month vs. Historical Benchmarks

NOTE: The historic low and historic high are based on the timeframe from the Index’s baseline of Q1 2021’s monthly average.

Opportunistic Investors Circle as More Assets Move into Play

CRE transaction activity has inched up every month since March and despite a small (and expected) dip in August, the buyer base is expanding, interest in evaluating opportunities is rising, and recent acquisitions have surfaced across all property types and geographic regions. Although there is much talk of distressed properties as a potential investment opportunity, transaction volume is still relatively low, but on the rise.

With each passing month, the reality of the challenges associated with maturing loans comes into sharper focus. Owners and lenders are left with tough decisions about refinancing with potentially steep capital infusion requirements, the possibility of loan extension, or forced sales. Foreclosures are still low which disappoints opportunistic investors with dry powder looking to pick up cheap assets in fire sales.

Signs of a market mobilizing to address what could be a dramatic transfer of assets are evident. LightBox data on the number of non-disclosure agreements (NDAs) per property listing are rising, a sign of willing buyers exploring new opportunities to place capital, particularly in the multifamily and retail sectors. Recent dealmaking cuts across all asset classes and all geographies. For properties that are performing, there is pent-up demand to sell at slightly increasing prices. In office, transferring of assets has already begun, some from forced sales, some from institutional investors opting to exit office and private equity buyers looking for opportunistic plays. Recent headlines suggest that new Class A buildings in strong metros are becoming attractive leasing options, with some companies even expanding their office footprint.

Summer dealmaking activity across all asset classes and geographies is evidence that a growing universe of investors is willing to pull the trigger on deals in a way that the market wasn’t seeing last year at this time. If the current recovery follows past patterns, investors will begin to deploy capital quickly once the rate cutting phase gets underway and they sense that the window of opportunity is open.

Market Mobilizes as Anticipation of a Busy Q4 Builds

The relative strength of the August CRE Activity Index, particularly compared to last August, positions the market for a strong 4th quarter. With inflation finally stabilizing near the 2% Fed target rate, interest rate cuts are around the corner and recently redrawn market forecasts are only adding to the optimism. The Mortgage Bankers Association, for example, revised its forecast and is calling for a promising 26% jump in CRE lending this year to $539 billion over $429 billion last year. The projected increase is driven by the expectation of several rate cuts, as well as a steady stream of loan maturities driving a long-awaited rebound in lending activity.

While traditional CRE lenders focus on minimizing their risk exposure by divesting non-performing loans and addressing refinance requests on the billions of dollars in maturing loans, they remain cautious about new loan originations. Private equity debt lenders and life insurance companies are ramping up and moving in to fill the bank lending gap.

Gray Clouds in the Near-Term Forecast

As the market prepares for an important pivot point in debt capital markets, hope for a busy 4th quarter springs eternal, but the near-term forecast is not without its gray clouds. Among them are growing concerns about a softening in the labor market which could signal that a recession is ahead. July’s job openings hit their lowest levels since 2021 so future metrics on employment numbers will be closely watched for potential red flags. The latest round of retail sales was also somewhat troubling as they show early signs that once-strong consumer spending could be losing steam.

The Fed is in a delicate position balancing the need to keep inflation close to 2% and unemployment at or around 4%. Employment and inflation reports, particularly leading to the presidential election, will be among the most closely watched metrics for any signs of concern, like reduced consumer spending, higher prices, a spike in layoffs or a decline in job listings that might signal a slide into recessionary conditions.

Watching for Market Reaction to Rate Cuts

The August LightBox CRE Activity Index reflects the underlying strength and resilience in the market, built on a foundation of growing momentum drawn from the recent stabilization in property prices, modest value increases in some asset classes, and a widespread mobilization of capital—all in the midst of unpredictable jolts of volatility in the broader economy. The September Index will reflect the market’s early reaction to the first rate cut, which will represent a small but important step away from the days of higher interest rates negatively impacting transactions, property values and borrowing costs.

While cuts won’t solve all of CRE’s problems, past experience shows that when rates decline particularly after a protracted period of historically high rates, CRE activity picks up quickly. “September has a reputation for being bearish,” observed Manus Clancy, LightBox Head of Data Strategy, “but investors seem teed up to pull the trigger on transactions in a way that we haven’t seen yet this year. After the first rate cut, I expect the types of dealmaking we’ve been highlighting in the CRE Weekly Digest podcast will only accelerate.” Despite concerns about reduced consumer spending and a weakening labor market, there are strong reasons supporting the position that September and Q4 will bring more positive momentum for CRE.

ABOUT THE MONTHLY LIGHTBOX CRE ACTIVITY INDEX

The LightBox Monthly CRE Activity Index is an aggregate that represents a composite measure of movements across activity in appraisals, environmental due diligence, and commercial property listings as a barometer of broad industry shifts in response to changes in market conditions. To receive LightBox reports, subscribe to Insights.