Capital Keeps Moving Through Uncertainty

According to the latest LightBox Transaction Tracker report, commercial real estate (CRE) transaction activity remained remarkably steady in April, signaling a market that continues to transact despite geopolitical uncertainty, elevated rates, and cautious capital markets.

April closed with 1,270 deals totaling $22.1 billion, a modest decline from March’s revised volume that appears driven more by a shorter calendar than any meaningful softening in demand. Four consecutive months of consistent deal counts point to a market that has largely adapted to today’s operating environment: lending remains available, capital is active, and investors continue to find opportunities across sectors.

Large transactions moderated further, but importantly, they appear to be stabilizing rather than disappearing. Deals above $50 million have settled into a narrower range since January, with the $50–100 million segment showing particular resilience. In a higher-rate market, deals in the under $100M OR nine-digit threshold are proving easier to finance, underwrite, and execute, creating an active proving ground for price discovery and disciplined capital deployment.

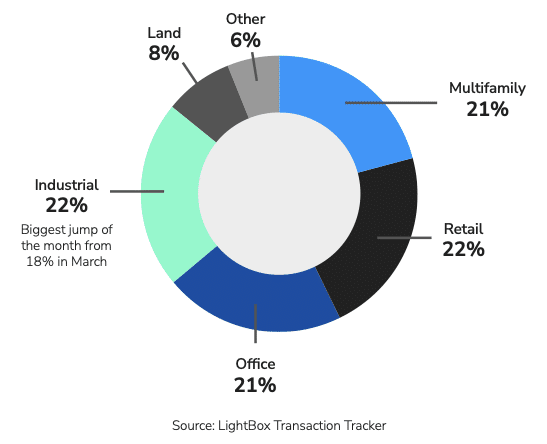

Across property types, April reflected a notable level of balance. Industrial (22%), retail (22%), multifamily (21%), and office (21%) each captured nearly identical shares of transaction activity, reinforcing the idea that investors are not retreating toward a single “safe” sector. Instead, capital is spreading across the market, with industrial’s rebound—driven by logistics, warehousing, and digital infrastructure—standing out as one trend to watch. Land transactions and specialty sectors including healthcare, hospitality, and senior housing added further diversification to the month’s deal mix.

April’s headline transactions tell an equally compelling story about where the market stands today. Office assets dominated the month’s largest deals, spanning both premium urban towers and distressed repositioning plays. Major office trades in Manhattan, Los Angeles, and San Francisco suggest that office price discovery is moving from stalemate toward execution, as buyers increasingly transact at reset values. Multifamily remained a strong institutional target, while industrial, retail, and land transactions reinforced the breadth of investor appetite across asset classes.

The broader takeaway: this is a market operating with disciplined optimism. Investors are moving beyond broad cyclical bets and focusing more intently on asset-level fundamentals, durable cash flow, local market dynamics, and underwriting precision. While macro uncertainty remains a factor, transaction activity continues to demonstrate that capital is still finding conviction — selectively, strategically, and with growing clarity.

Distribution of April Deals by Property Type

What You’ll Find in the Full Report:

- A detailed breakdown of April deal volume and transaction value trends

- Analysis of large-deal stabilization and shifting transaction composition

- Property-type insights across industrial, retail, multifamily, office, land, and specialty sectors

- Highlights from April’s largest transactions and leading buyers

- Market observations on price discovery, underwriting trends, and investor behavior

- Forward-looking perspective on CRE resilience, capital deployment, and second-half market dynamics

Download the full April LightBox Major CRE Transaction Tracker report for a deeper look at where capital is flowing, who’s driving activity, and how investors are navigating today’s evolving market environment.